Hurdles and promises of green ethylene production in the UK

Executive Summary: Light olefins, comprising ethylene and propylene, are fundamental building blocks in the chemical industry for the production of plastics, synthetic fibres and synthetic rubbers. In the UK alone, the annual olefins production amounts to 2.75 Mt and emits 3.1 MtCO2, making it the most emission-intensive process across the UK’s chemical sector (~17% share, equivalent to ~0.5% of the UK’s total greenhouse gas emissions in 2019). Techno-economic and environmental life-cycle assessments conducted by the Centre have shed light on the main opportunities and challenges towards displacing steam crackers for green ethylene from CO2.

The challenge: Olefins production is particularly challenging to defossilise since fossil fuels are not only used to meet the utility demands, but also supply the carbon feedstock itself. Of the alternative candidate feedstocks, sustainably-sourced lignocellulosic biomass is currently in limited supply, with DESNZ recommending its prioritisation for negative emission technologies.[1] Challenges with polymer recycling arise from the feedstock heterogeneity and availability,[2] as well as quality loss with mechanical recycling and catalyst deactivation caused by additives and impurities in chemical recycling. By contrast, CO2 can be captured from industrial processes or extracted from the atmosphere and purified for its utilization. The UK has large CO2 storage capacities and aspires to become a global leader in carbon capture, utilisation, and storage (CCUS).[3] The industrial clusters around Merseyside and on the East coast (Teesside and Humberside) have set respective targets to capture 10 MtCO2 and 27 MtCO2 annually from industrial point sources from 2030. Nevertheless, CO2 from industrial processes and power plants remains ultimately linked to fossil fuel consumption. Following the terminology applied to hydrogen production processes,[4] only a production route based on direct air capture (DAC) and powered by renewable energy may be considered truly green.

Supplying CO2 utilisation pathway with green electricity and hydrogen would call for a major expansion of the UK’s renewable power generation capacity. A whole systems perspective is much needed to account for the limitations on renewable generation capacity due to land availability, cost and public acceptance.[5] However, current scenarios for the UK’s future energy system fail to reflect these additional demands, due in part to the difficulty of integrating chemical production processes into whole-system energy modelling. Deciding early on a decarbonisation strategy across different sectors is paramount to reducing the overall system costs associated with the transition to net-zero by 2050.

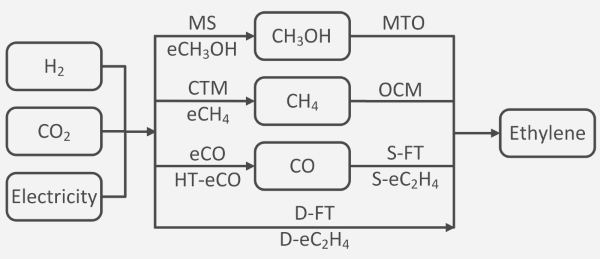

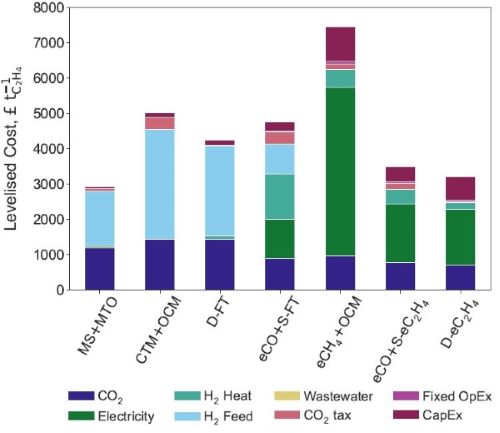

Results obtained at CircularChem: In response to these challenges, the team at Imperial College London set out a comprehensive techno-economic assessment of potential green ethylene production routes from air-captured CO2 and renewable electricity (Figure 1), with a particular focus on technology readiness for deployment by 2035.[6] This modelling predicted that the levelised cost of ethylene (Figure 2) will be lowest for the methanol-to-olefins pathway (£2900 per ton), followed by fully-electrocatalytic routes (£2900–3200 per ton). Process routes relying on Fischer-Tropsch synthesis or oxidative coupling of methane were furthermore predicted to be uncompetitive in their present state of technology. By and large, a green ethylene price of three times or more of its current market price (~ £1000 per ton), backed up by a sensitivity analysis, provides a clear incentive for intensifying R&D efforts on catalyst and process innovation for CO2 utilisation.

Naturally, one of the main motivations behind replacing fossil-based ethylene with green ethylene lies in the prospect of producing carbon-negative ethylene and co-products (from a cradle-to-gate viewpoint). The modelling conducted by the Centre also confirmed that the allocated net emissions per tonne of green ethylene produced could be as low as −3.3 tCO2-eq and −1.9 tCO2-eq for the MTO and direct CO2 electroreduction routes, respectively. So both thermocatalytic and electrocatalytic routes would indeed present a negative carbon balance from a cradle-to-gate point of view. On the path to net-zero, this would allow for a dramatic reduction over conventional ethane steam crackers, whose cradle-to-gate emissions are estimated to exceed +3 tCO2-eq per tonne of ethylene. As an interim solution, ethylene production will likely continue to rely on fossil feedstock but could be retrofitted with CCS or hydrogen as fuel to lower its emission intensity.

.

Figure 1: processes and intermediates in the conversion of CO2 to ethylene. Abbreviations: MS: methanol synthesis; eCH3OH: CO2 electroreduction to methanol; MTO: methanol to olefin; CTM: CO2 methanation; eCH4: CO2 electroreduction to methane; OCM: oxidative coupling of methane; eCO: CO2 electroreduction to CO; HT-eCO: high- temperature CO2 electroreduction to CO; S-FT: syngas Fischer-Tropsch; S-eC2H4: CO electroreduction to ethylene; D-FT: direct Fischer-Tropsch; D-eC2H4: CO2 electroreduction to ethylene.

Figure 2: Levelised cost of ethylene and corresponding breakdown for green ethylene routes from CO2.

Wider implications and working with partners: At the time this assessment was conducted, all three ethane steam crackers in the UK were still reliant on shale gas imports from the US. While CO2 utilisation for green ethylene production would promote the use of local resources such as offshore wind power, a major impediment to deployment lies with the huge demand for renewable electricity. The modelling conducted by the Centre predicts that displacing the ethane cracker in Wilton, Teesside (capacity of 800 ktpa) could consume as much as 41–52 TWh of electricity, without including the electricity needed to power DAC. These demands correspond to 13–16% of the UK’s total electricity generation in 2022 (325 TWh of which c. 40% comes from renewables) for a single cracker. For comparison, the ethane cracker in Wilton consumes 11.5 TWh per annum in total, a much smaller share (~3.5%) of the UK’s annual electricity consumption.

Alongside the huge demand for renewable energy to power green ethylene comes the physical footprint of a dedicated off-shore wind farm, larger than the area of Greater London. Such figures

put a clear pressure on the chemical industry to take a strategic decision on securing its supply of low-cost, low-carbon electricity. Delaying this decision could put the industry at risk of missing out on the best offshore wind farm leases, as the seabed areas in the UK exclusive economic zone (EEZ) are continuously auctioned. In the context of low-carbon ethylene production, the chemical

industry might want to reconsider the idea of co-locating future chemical plants with nuclear plants that could supply both heat and power.[7]

The centre has been collaborating with the North East of England Process Industry Cluster (NEPIC), enabled by Innovate UK funding, towards the creation of a sustainable olefins supply chain on Teesside. Leveraging the techno-economic assessment on green ethylene from air-captured CO2, a complementary techno-economic assessment was conducted on the production of bioethylene from bioethanol (biomass route), which identified similar benefits in terms of reducing CO2 emissions (c. −4 tCO2-eq per ton of bioethylene due to biogenic CO2 origin) while predicting a competitive bioethylene production price when the ethanol price is low. All the know-how acquired on techno-economic and life-cycle assessment of green ethylene is furthermore being leveraged through consultancies with SMEs, such as OxCCU Ltd on the production of sustainable aviation fuels from captured CO2 and green hydrogen.[8]

References:

[1] Department of Business, Energy and Industrial Strategy (2021), Net Zero Strategy: Build Back Greener.

[2] The European Technology Platform for Sustainable Chemistry (2020) Sustainable Plastics Strategy.

[3] Department of Business, Energy and Industrial Strategy (2022) Carbon Capture, Usage and Storage.

[4] Velazquez Abad & Dodds (2020) Green hydrogen characterisation initiatives: Definitions, standards, guarantees of origin, and challenges. Energy Policy 138(C).

[5] Kätelhön, Meys, Deutz, Suh & Bardow (2019) Climate change mitigation potential of carbon capture and utilization in the chemical industry. PNAS 116(23):11187.

[6] Nyhus, Yliruka, Shah & Chachuat (2024) Green ethylene production in the UK by 2035: A techno-economic assessment. Energy & Environmental Science 17:1931-1949.

[7] Leonzio, Chachuat, Shah (2023) Towards ethylene production from carbon dioxide: Economic and global warming potential assessment. Sustainable Production & Consumption 43:124-139.

[8] Bernardi, Casan, Symes, Chachuat (2023) Enviro-economic assessment of sustainable aviation fuel production from direct CO2 hydrogenation, Computer Aided Chemical Engineering 52, 2345-2350.

Researchers: